New Markets Venture Partners’ Latest Edtech Fund Closes at $68 Million

By Tony Wan

May 16, 2018

retrorocket / Shutterstock

When New Markets Venture Partners first began fundraising for its second education technology investment fund, Barack Obama was in office, Brexit was for up for debate and iPhones still had headphone jacks.

Now, more than two years later, New Markets is finally calling it a wrap. Its latest fund, dubbed “New Markets Education Partners II,” formally and finally closed on April 30, totalling $68 million.

The firm plans to invest up to $5 million into Series A, Series B and recapitalization rounds for education companies serving pre-kindergarten to professional learners, with a focus on digital learning, learning sciences, analytics and workforce development services.

Already, roughly 15 percent, or about $10 million of the fund’s $68 million total, have been invested across seven companies: Credly, LearnPlatform, Motimatic, Noodle Partners, Pairin, Practice and Signal Vine. The firm aims to invest in up to another seven U.S. companies over the next five years, and it has set aside a portion to support follow-up investments should a company decide to raise future rounds.

It may have felt like a different world when New Markets began fundraising in January 2016. But while the process may have seemed unusually long, that was not unexpected, according to Jason Palmer, who joined New Markets as a general partner that November.

Part of the reason, he said in an interview with EdSurge, was that New Markets took a “counterintuitive approach to raising money” that bucks conventional tech-investing wisdom. “We don’t focus on San Francisco and New York companies, but on cities that are off the beaten track,” he says. Making that pitch to funders, Palmer adds, “required a certain amount of persuading to show that the best education companies come elsewhere.” (Still, three of the New Markets’ seven investments from this fund are based in one of those startup hotspots.)

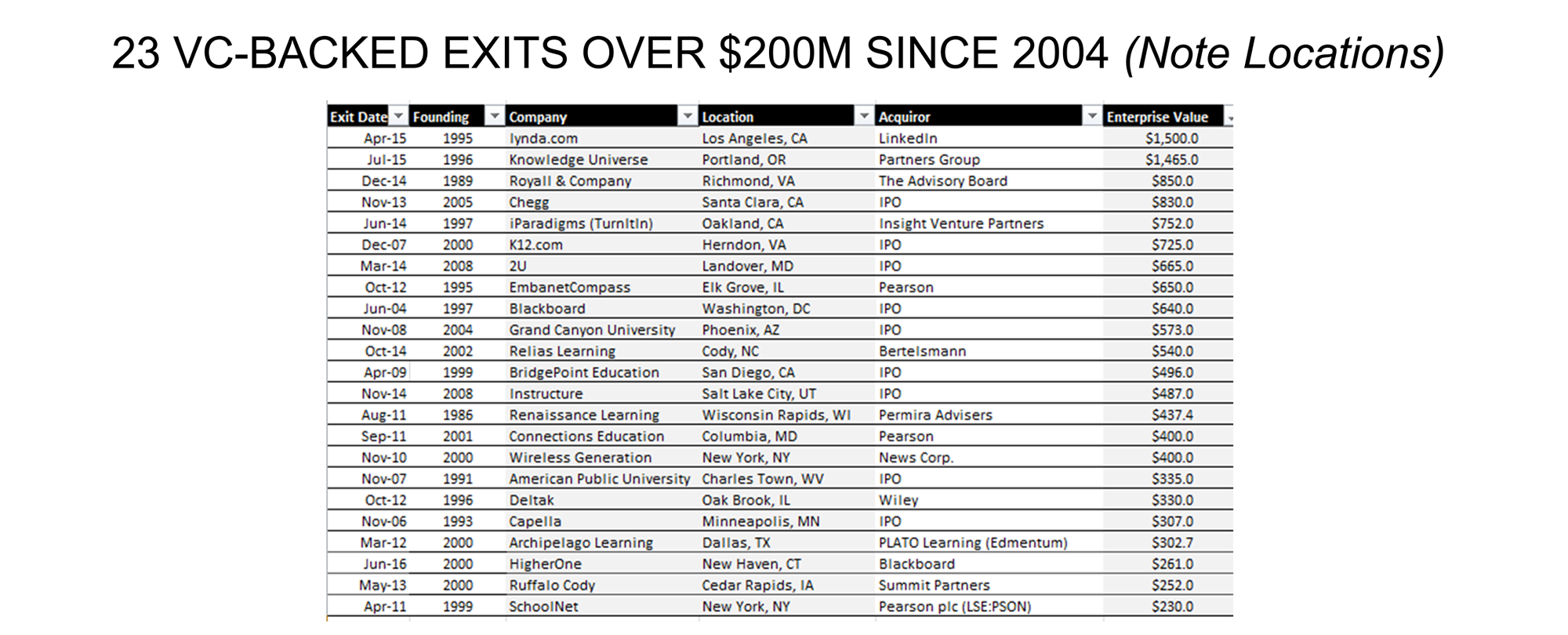

It’s a bold, but not entirely unfounded, thesis. The mid-Atlantic region near New Markets’ headquarters in Fulton, Maryland is home to some of the education industry’s biggest names, including Blackboard, EverFi, Laureate Education and 2U. And according to Palmer’s research, 21 of the 23 largest exits in the edtech industry have come from companies based outside of New York or the San Francisco Bay Area.

The backers for New Markets’ latest fund hail from a broad geography as well, including Iowa-based ACT (which contributed $10.5 million), Lumina Foundation and Strada Education Network (both based in Indianapolis), ECMC Group (headquartered in Minnesota) and Newark-based Prudential Financial.

This marks the second time that Lumina and Strada have supported a New Markets investment fund. (They last did so in 2013.) For Brad Kelsheimer, Lumina’s vice president and chief financial officer, this effort supports the nonprofit’s aim to achieve market-rate investment returns from companies that align with its mission to support postsecondary learners. The partnership also helps surface new tools and services. In 2016, both New Markets and Lumina invested in Credly’s seed round—marking Lumina’s first direct investment in a for-profit company.

It also gives the foundation a lens into the challenging realities of the edtech startup ecosystem.

“The biggest thing we’ve learned is the long incubation period for seed-stage investments to grow, Kelsheimer says, “and the fact that it’s a very slow sales cycle into the traditional higher education system.”

New Markets’ Market Forecast

Over the years, New Markets’ Palmer, whose career includes stints at Microsoft, Kaplan and the Gates Foundation, has learned to read market cues from federal legislation. In an op-ed reflecting on his career in the education industry, Palmer wrote that “policy’s invisible hand can be 10 to 100 times more powerful than Adam Smith’s free market.”

Today, he believes that the Every Student Succeeds Act is the latest linchpin policy to shape the K-12 market. By raising the bar for “evidence-based” interventions and educational services, ESSA “requires school districts to be much more deliberate and intentional about adopting products with proven efficacy,” Palmer says. That means that “the companies we invest in are efficacy-focused and engaging in third-party studies to make sure the products work.”

Palmer also points to the Workforce Innovation and Opportunity Act as another driver of innovation—and federal funding—for career-related services. In particular, he’s smitten with how learners will be prepared for the emergence of “new collar” jobs (a term often attributed to IBM CEO Ginni Rometty) in industries that require technical training but not necessarily a traditional four-year degree.

“There is a huge skills gap in what companies want for middle-skilled positions,” he says, that represents an opportunity for companies and schools to provide that training—even for high school graduates who may eschew the four-year college path.

In light of these opportunities, Palmer maintains that New Markets is a “valuation-conscious investor and focused on investing in companies at rational valuations.” What he steers clear of are those companies that attract “stratospheric” interest without strong supporting financials.

That discipline also requires keeping an eye out for investment gaps. At a time when investors seem to have cooled off from K-12 deals, Palmer notes, the firm “will focus more in K-12 because it’s not very crowded anymore.” One deal that’s in the works, he teased, is a startup focused on STEM and computer science.

With measured expectations come measured results. New Markets’ may not have reaped the windfall returns that many tech investors swoon over, but it has seen eight exits over the past six years. Acquired portfolio companies include Starfish Retention Solutions (by Hobson’s), Moodlerooms (by Blackboard), ThinkThrough Learning (by Imagine Learning), and Practice (by Instructure). The only acquisition with a disclosed valuation was Questar’s $127.5 million sale last year to Educational Testing Service.

To date, New Markets has invested nearly $30 million across 23 education technology companies since its founding in 2003.

At a time when many venture capital firms tout and celebrate the valuation of companies in their portfolios, “we gauge our success on cash exits and returns to our limited partners,” Palmer quips. Given that New Markets has tapped previous investors to re-commit to this new fund, it seems like their backers should have reason to be optimistic.

Tony Wan (@tonywan) is Managing Editor at EdSurge.

Popular on Edsurge

Voices of Change