Chinese Edtech Sees $1.86B in Q1 2019, Bucking Plummeting Venture Trend

By Siyi Zhang

May 27, 2019

hxdyl / Shutterstock

In China, the edtech industry appears to be immune to the whiplash that has hit venture investing across other sectors.

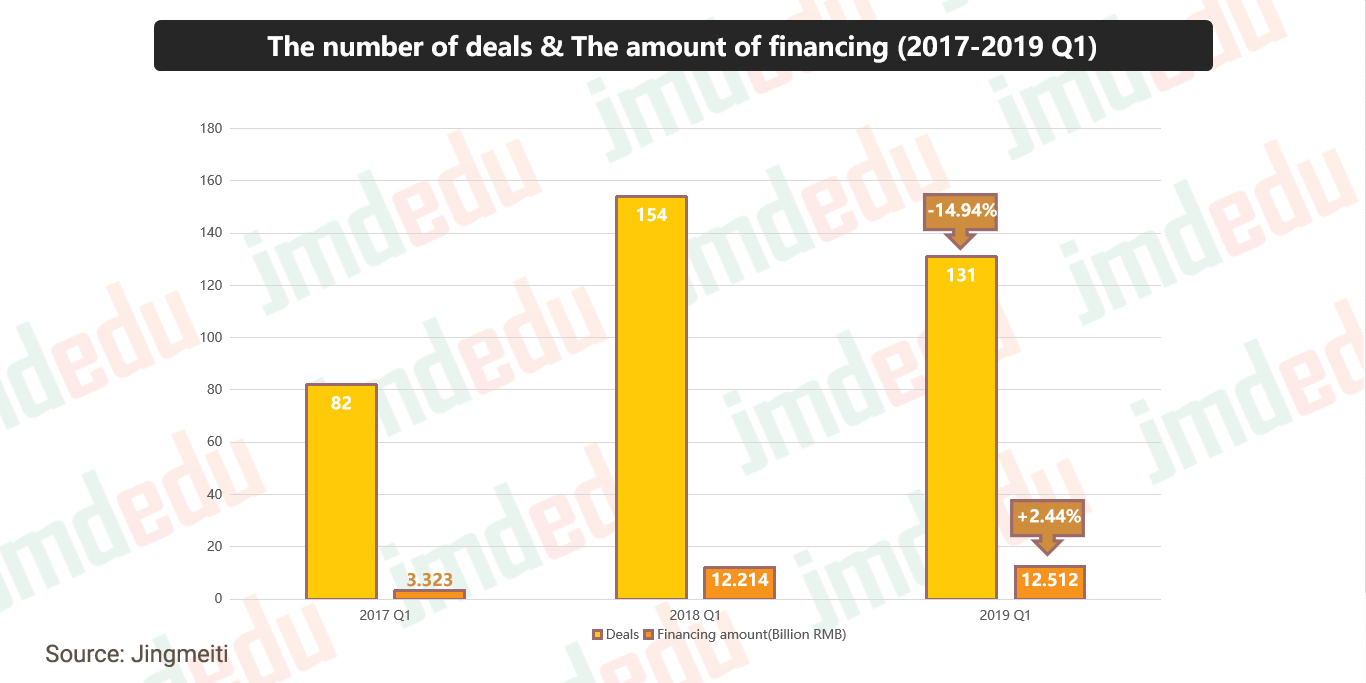

Education investments showed modest growth in the first quarter of 2019, even as venture investing in China in all other sectors dropped sharply. From January through March 2019, 131 China edtech ventures raised more than $1.86 billion (RMB 12.51 billion), according to data compiled by Mission EDU and Jingmeiti. That represents a year-over-year growth of 2.4 percent increase in financing.

By contrast, venture investing overall in China dropped 87 percent to $35.9 billion (RMB 241 billion) in contrast to a year earlier, according to a recent report by the Chinese Academy of Science and Technology.

Within the Chinese education sector, three sectors saw a concentration of investments:

competency-based education;

language learning;

education “informazation.”

Investors put their money into 29 competency-based education companies—or almost a quarter of all the edtech investments—during the first quarter. Here are some highlights:

In the K-12 sector, Zhangmen, a one-to-one online tutoring system that uses teachers who are graduates of China’s top institutions including Tsinghua and Peking University, completed a $350 million Series E round of financing. Huohua Siwei (火花思维), an online children’s “thinking training platform” ranked second, completing a $40 million Series C round. And VIPThink (豌豆思维) secured a $15 million Series A round to further develop its STEM platform for preschool students. Huohua Siwei and VIPThink similarly offer online platforms to strengthen children’s mathematical thinking.

In the language-learning market, Dada raised $255 million in its Series D round. The other top five deals in this subsector—with one exception–are online English-learning platforms: Putao English (angel round), Acadsoc (Series C1) and MicroLanguage (Pre-B round). The exception is Meten English, which offers offline English courses.

“Education informatization” is a broad idea outlined by the Chinese government in April 2018 that aims to establish “one big” internet and education platform that encompasses technologies and apps that drive learning for students and professional development for educators.

Overall, online education platforms are growing fast and consumed about half of the large-scale funds in Q1 of 2019.

Also notable: Investments in vocational education is the fourth largest category in the Chinese education market and is expected to continue to develop during the second quarter of 2019. All deals in vocational training amounted to about $593 million, or a third of the financing in the edtech sector during the quarter. But slightly more than half of that activity was wrapped up in the acquisition of Saipu Training, which sold for $311 million. Sapiu Training provides personal trainers and customized courses for working out in gyms.

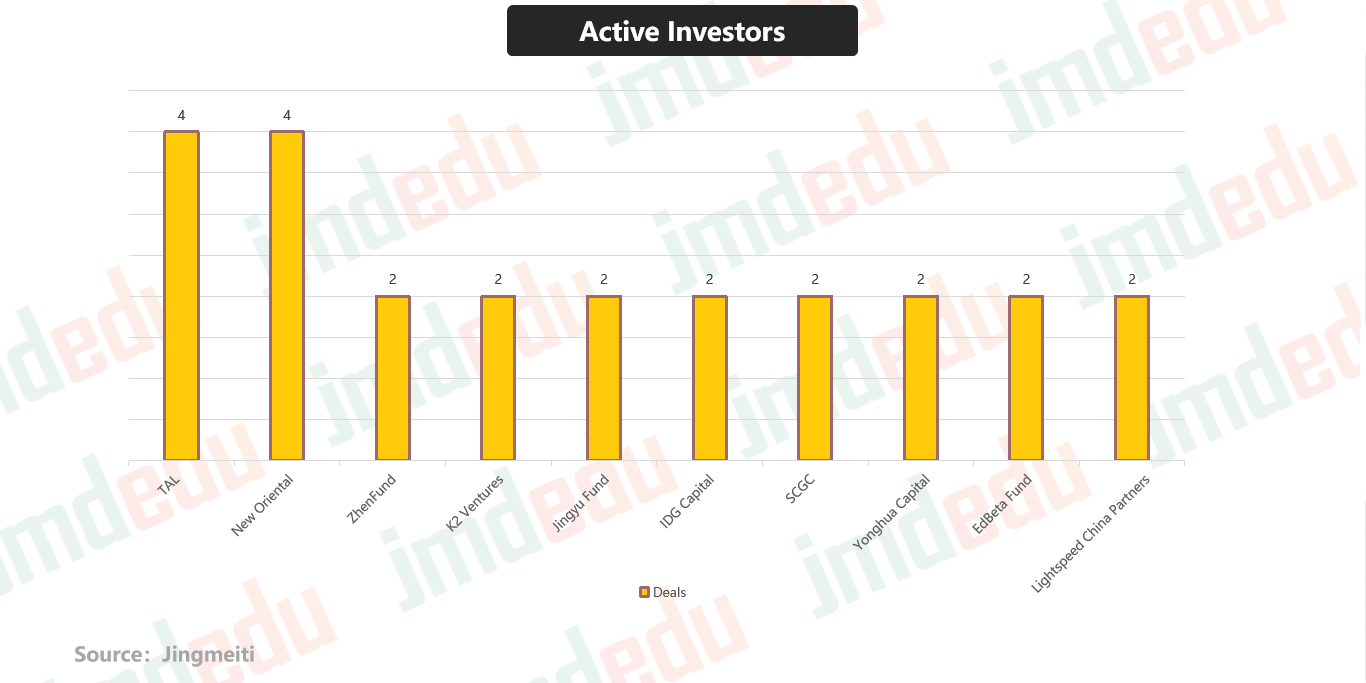

TAL Education Group and New Oriental have been the most active investors, with both closing four deals during the first quarter. New Oriental had a prominent presence at the ASU GSV 2019 Summit this past April, where it presented a session called “China Pop Up,” aimed at helping investors decode China’s education market. During the session, New Oriental leaders announced their long-term strategic partnership with ASU GSV to develop more East-West cooperation opportunities.

On the Rise: ‘Big Chinese Learning’ & Kids Coding

One of the most significant factors contributing to the growth of deals in competency-based education is a new trend dubbed “Big Chinese learning (大语文).” This term refers to an approach to comprehensive Chinese language training that combines both liberal arts teaching and the traditional exam-oriented model.

Industry leaders are bullish about the trend. “The ‘Big Chinese’ field will definitely breed the next unicorn,” said Yu Minghong, the founder of New Oriental. Even though most of the companies in this sector are still early stage, edtech investment gurus are hot on this path: Blue Elephant Capital, Northern Light Venture Capital and TAL Education Group are all considering new investments in this field.

Three of the biggest recent deals in competency-based learning have gone to companies that support teaching students to code: Hetao101 (Series A+ round worth $17.4 million), Codemao (Series D round totaling more than $14.5 million) and Xiaomawang (Series B round with $1.4 million). But these investments are still high risk in China. Teaching students to code is still not in high demand by most Chinese parents. Rather, this market tends to be more focused on tapping students’ potential or even cultivating soft skills.

At the moment, the market size for coding is estimated to be around $435 million to $580 million. That means there is a huge gap between demand for student coding programs and teaching students English, which is estimated to be a $8.7 billion market. Nationwide, the market penetration of coding education programs is only about 1.5 percent. But in the future, as more top-down policies favoring these skills are carried out, the coding market is predicted to reach $4.3 billion in five years.

As we wrote in our previous article, “Decoding 2018 China’s Education Market,” small online classes are also expected to become a major trend. Many one-to-one online teaching companies have begun to transform their business models to deliver small-class instruction, hoping to improve their marginal costs. Even so, there are many complicated steps in moving to a small-class model that could increase operation costs. How robust these evolving business models are remain to be seen.

Siyi Zhang is an intern editor at JMDedu.

Editor’s note: This article was produced through a partnership with JMDedu, which is an investor in EdSurge. JMDedu also manages the GET Edtech Summit & Expo. See here for more up-to-date news and stories from JMDedu.

Popular on Edsurge

Voices of Change