Campus Closures. What’s Tech Got to Do With It?

By Greg Jackson

August 9, 2018

CC BY 2.0 acidpix / Flickr

A version of this article first appeared on Greg Jackson’s LinkedIn page.

Coleman University is closing, as I read recently in my local paper, the San Diego Union Tribune. It’s not alone: the parent company that owns the for-profit Argosy University and Art Institutes, Dream Center Education Holdings LLC, is “discontinuing campus-based programs” at seven of its campuses in California.

The rating agency Moody’s believes that about 15 colleges or universities will close each year. They don’t predict exactly which, although a recent Washington Post article explores some examples. While Moody’s predictions have generally proven to be a smidge pessimistic, institutions are certainly dying.

Yet last year was a big one for edtech investment, according to Daniel DelaCruz of Dualboot Partners. “Internationally, the market shattered its own funding record, with 813 different companies landing a total of $9.52 billion in investment. In the U.S. alone, educational technology companies raised $1.2 billion. Those numbers verify something we’ve known for a long time,” DelaCruz concludes, “Edtech has serious potential—both for entrepreneurs who know the pain points and investors looking to tap into a growing market.”

Some of this investment will be conventional—computer-lab renewal, classroom technology, network upgrades and such. But some of it, Diana Oblinger observes in a recent eCampus News article, “may prompt us to re-conceptualize education in a world of lifelong learning and partnerships with smart machines.”

Juxtaposing the shuttering campuses, the investor enthusiasm in edtech, and predictions of a change in the culture of education suggests a question:

Is educational technology preventing institutional closures, promoting them, or compensating for them?

Educational technology investments can affect colleges and universities in different ways, as I've elaborated elsewhere. For example, investments in educational technology can do one or more of the following:

help institutions innovate and otherwise improve what they already do by enabling better or more expansive learning,

enable institutions to reach new clienteles, especially by using technology to provide online education far beyond their campus boundaries, thereby possibly increasing their revenues, or

reduce institutional costs by streamlining administrative or academic processes (or both)—and possibly replacing expensive staff with less expensive technology.

How might these roles play out in the context of campus closures? To explore this, I’ll start with a selective overview of higher-education demography and the ensuing challenges, and then consider a couple of examples.

Closures

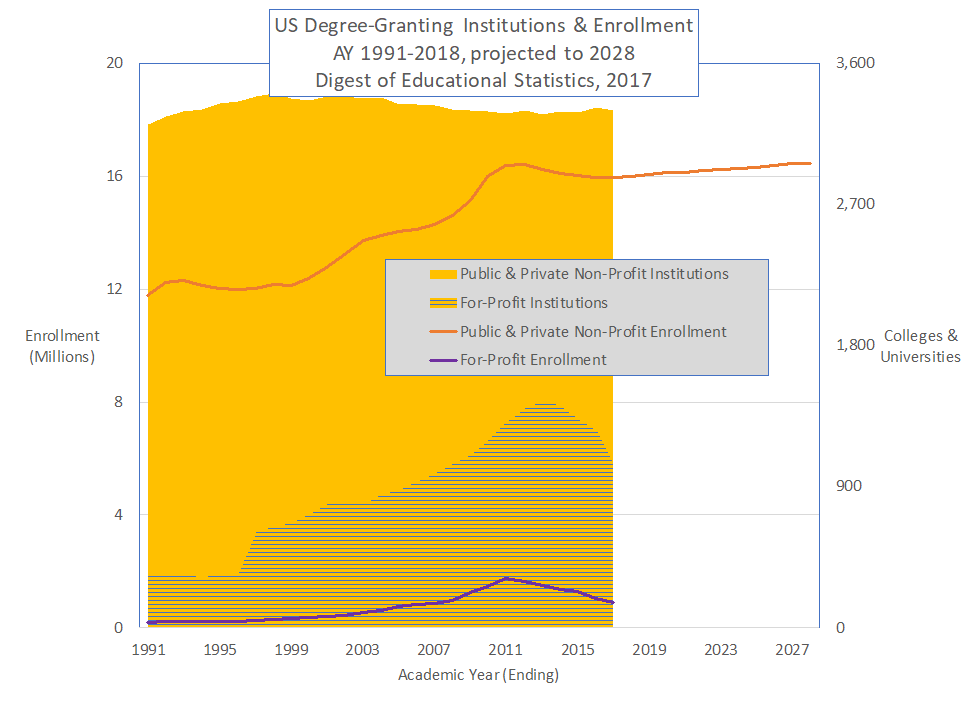

As the graph below shows, college closures aren’t a brand new trend. According to the US Education Department IPEDS surveys, the largest number of public and non-profit private campuses was 3,393, in 2001. The largest number of for-profit campuses was 1,451, in 2013.

Between 2000 and 2017 (the most recent year available), the number of public and private non-profit campuses shrank by about 40. The number of for-profit campuses doubled to 1,451 before shrinking back to 1,055.

Enrollments don’t explain the pattern. In public and private non-profit campuses—the yellow and orange portions of the graph—enrollments grew, even as the number of institutions shrank. In for-profit campuses—the purple parts—the number of institutions grew much more sharply than enrollments, and then fell likewise. Then, since 2011, enrollments shrank a bit, but the number of public and non-profit institutions continued to grow.

The National Center for Educational Statistics projects that enrollments will increase a bit over the next decade—although there will be underlying changes, primarily part-time, multi-institutional, working-student and other so-called “nontraditional” modes of study.

Why are we losing campuses?

The central issue is that there are lots of small campuses, and small campuses are at unique and increasing risk. Although each closing has distinct particulars, the core problem for campuses at risk is finances.

A few years ago Bain, the management-consulting firm, analyzed college and university balance sheets, revenues, and expenditures in the US, and estimated that about 20 percent of campuses were likely to become insolvent. Deferred maintenance, selling assets, spending down reserves and other one-time tactics could stave off insolvency for a while, Bain suggested, but could not change the fundamental trends.

As I’ve observed elsewhere, all seven of the standard funding sources for higher education are under pressure—state appropriations, federal financial aid to students, students’ and parents’ ability to pay, eleemosynary support from foundations and private donors, federal research and other direct funding for campus operations, corporate support and investment yields.

Small institutions are especially vulnerable, since they are typically private, and their revenues consist primarily of tuition from and financial aid to students.

Small institutions have few ways to compensate for shrinking revenues—for example, by deferring maintenance. They accumulate deficits or debt, have no way to offset or pay these, and this puts them at much greater risk than larger institutions.

This, rather than student demographics or competition from for-profit institutions, lies at the heart of the warnings by Bain and Moody’s.

What about students?

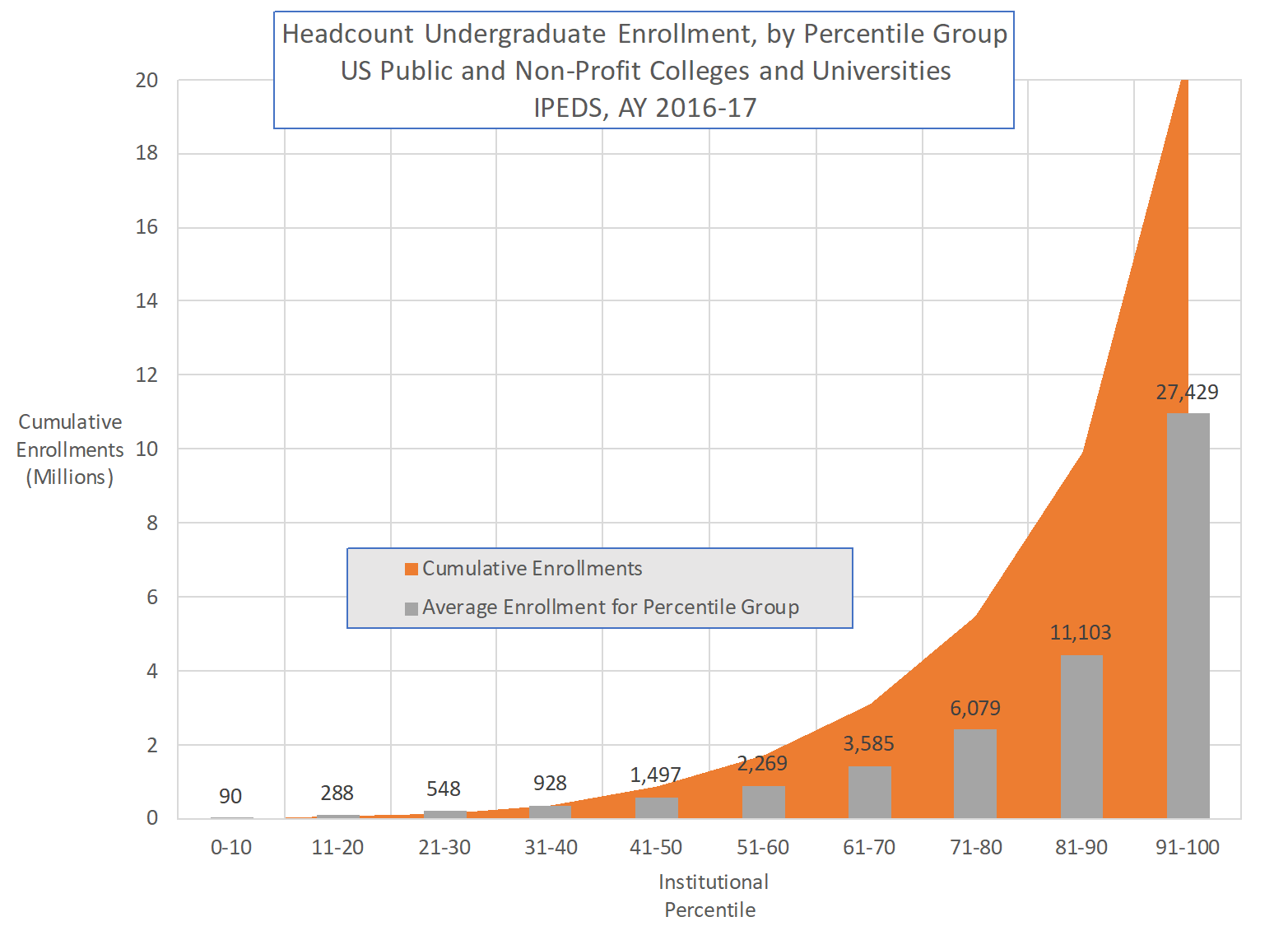

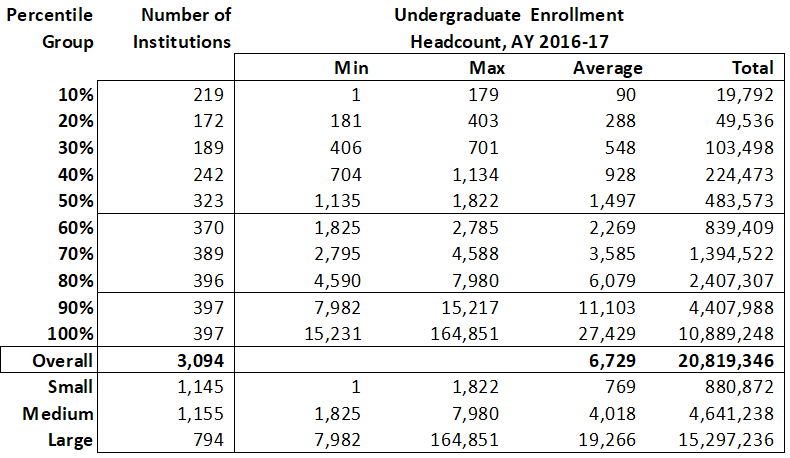

Moody’s and Bain predict that we will continue to lose institutions, and at an increasing rate. But the effect on students will be smaller. Here’s why: Although small campuses account for a large fraction of the institutional universe, institutional size comes very close to a Pareto distribution—the largest 20 percent of campuses account for 73.5 percent of enrollment—and so small campuses account for a very small fraction of the student universe.

The graph below illustrates this, showing average and cumulative enrollment for campuses with undergraduate students, broken out by decile: the smallest half of all campuses, for example, accounts for only 880,872 students or 4.2 percent of total enrollment.

Taking that as a starting point, consider a simplistic but illustrative analysis based on the Bain/Moody predictions. Let’s focus on undergraduates in public and non-profit institutions, and assume that the projected 20 percent insolvency rate consists entirely of colleges and universities in the smallest size group—those in the 10th through 50th percentiles, with 1,822 or fewer students:

The simplistic assumption that only small institutions close suggests that 20 percent, or 619 small institutions, might be lost to insolvency, if Bain’s estimates are correct. That’s 54 percent of institutions in the Small group, so institutionally the effect would be enormous.

If losses distribute evenly across the group, losing over half of small campuses translates to 476,056 students affected. That amounts to 2.3 percent of all students in public and private non-profit institutions. A half million students is a lot, but it’s a number that larger campuses and online programs might well accommodate. More on that below.

Of course the simplistic scenario is just that, and so unlikely to be exactly what happens. Closures may not be confined to the Small group, enrollment impacts may not distribute evenly, Bain/Moody’s estimates might be off, some apparently “small” institutions may have lots of graduate enrollment, and so on.

But the general point remains: although closures are likely to have a major effect institutionally, their effect on students will be proportionally less severe.

Wait. Hasn’t IT helped some institutions cope?

For sure.

“If ever there were a metaphor for the impact of technology and demographic shifts,” the Chronicle of Higher Education’s Goldie Blumenstyk wrote recently, “it can be found at Fayetteville State University, which plans to demolish two rundown dormitories—and not replace them at all.” Fayetteville State, a 6,500-student historically black university (HBCU), is demolishing two unused dormitories as its students shift toward online and other nontraditional enrollment patterns. Blumenstyk finds Fayetteville’s story reassuring: “It’s gotten to the point,” she says, “where I almost (almost!) don’t bother to read the Moody’s higher-education reports.”

But there’s important nuance. Fayetteville State is using technology to adapt to its current clientele, rather than to expand its reach to new clienteles. So long as Fayetteville State is serving a well-defined, loyal constituency, it can expect IT investments to help it deal with its constituency’s evolving preferences and survive. The same is true for other institutions similarly situated, or for much larger and more general institutions that simply can afford more investment.

Moreover, Fayetteville State isn’t small. As Blumenstyk notes, smaller campuses may have neither the resources nor the success that Fayetteville State enjoys, and perhaps “won’t want or be able to make that kind of shift.”

For an institution with a well-defined clientele and sufficient size to free resources for innovation, IT can maintain solvency and keep the place in business. That’s much less likely for an institution with few resources, or whose clientele is ill-defined, declining, or overlaps with other, more stable (read: larger) institutions.

So IT can help, but in the most worrisome cases it probably won’t.

What happens to students in those worrisome cases?

“Penn State University is on the prowl in San Diego,” says another Union Tribune article, “searching for students willing to pay tens of thousands of dollars to earn a degree online. The University of Maryland is doing the same. So are Purdue, Old Dominion, Colorado State, Arizona State, the University of Arizona, Southern New Hampshire University and Grand Canyon University.”

Moreover, the San Diego region has several large, successful, inexpensive public community colleges also hungry for new students, since revenues from the state depend partly on enrollments (disclosure: I ran IT at one of those, the three-campus San Diego Community College District, in 2017). Not to mention San Diego State, the University of San Diego, and of course the University of California at San Diego. And the University of California Extension.

So students set adrift by closings at Coleman, Argosy, the Art Institutes, and elsewhere around San Diego have options. The same is likely true for students set adrift elsewhere, whether it’s another local campus or distance enrollment in an online program from afar. Displaced students probably won’t end up at another small college. But they mostly will end up at institutions likely to survive, educate them, and grant them degrees.

Overall this shift will impose only minimal burdens on the regional, state, and national higher-education systems, or on individual institutions. If the students set adrift by insolvency distribute proportionally across other institutions, then average enrollment at those surviving institutions would rise by an average of perhaps 3 to 4 percent. Especially because technology investments at larger and online institutions enable them to accommodate more students efficiently, this is unlikely to be problematic.

So is educational technology preventing institutional closures, promoting them, or compensating for them?

No, no, and yes—or so I believe.

So far as I can tell, except in exceptional cases, IT can’t solve institutional solvency problems. So techis not preventing institutional closures.

Likewise, the financial problems that Moody’s and Bain describe stem from imbalances among large-scale fundamentals such as salaries and benefits, tuition revenues, financial aid, facilities maintenance and depreciation and debt service, rather than from more marginal factors such as educational-technology investment. So tech is not promoting closures, except in one sense I note below.

But tech is compensating for institutional closures, by giving the affected students a growing array of options.

Over the past few years, educational technology has enabled higher education to evolve from a local and regional enterprise to a national one. It has done this partly by enabling institutions like Colorado State, Penn State, and the University of Maryland to offer instruction and degrees to online students far from their campuses; partly by enabling online-only multi-institutional collaborations like like edX and Coursera to exist and prosper; and partly by enabling national for-profit entities like the University of Phoenix to deliver highly standardized instruction efficiently across a huge array of physical venues.

By enabling this suite of national resources, educational technology helps mitigate the effects of institutional closures on students. In the process, it may encourage some threatened institutions to close rather than continue struggling, but I expect this effect is minimal. Moreover, it may well have encouraged new forms and structures for higher education to emerge, ranging from Western Governors University to edX.

IT investments may not be able to save institutions from insolvency. It’s important to recognize that fact, rather than to promote false institutional hopes.

But it’s also important to recognize that campus closures need not foreclose options for students, that IT plays a central role in ensuring that, and that wise investments in educational technology remain critical to the future of US higher education.

Greg Jackson is an IT leader, advocate and speaker, and a partner at Fortium Partners LP.

Popular on Edsurge

Voices of Change